Office demand is recovering, but it’s a different market. Class-A is nearly full, deliveries are at historic lows, and the developers paying attention are walking into an undersupplied market with three distinct entry points.

For the last five years, the office market has been on a rollercoaster. Shifting fundamentals, economic uncertainty and a turbulent capital market environment has defined the office sector for years.

This year, office should have fewer twists and turns. Office demand has started to recover significantly, particularly in major metros, helping to bring the market back into a supply-demand equilibrium. The market is showing promise of growth and an opportunity for new construction to reenter the sector. But commercial real estate developers are finding a much different market today. Office usage has changed and is continuing to evolve alongside labor and disruptive technologies, like AI, and occupiers are prioritizing different types of spaces and characteristics to accommodate modern work.

But in all of this change, there is opportunity. The office new construction pipeline has been quiet, but increasing demand will help drive down the vacancy rate. While this isn’t the time for overexuberance, office developers paying close attention to emerging trends and increasing demand will find space for new projects. Here is a closer look at where office fundamentals stand today, and where there is the most opportunity.

Office Fundamentals Are Looking Up

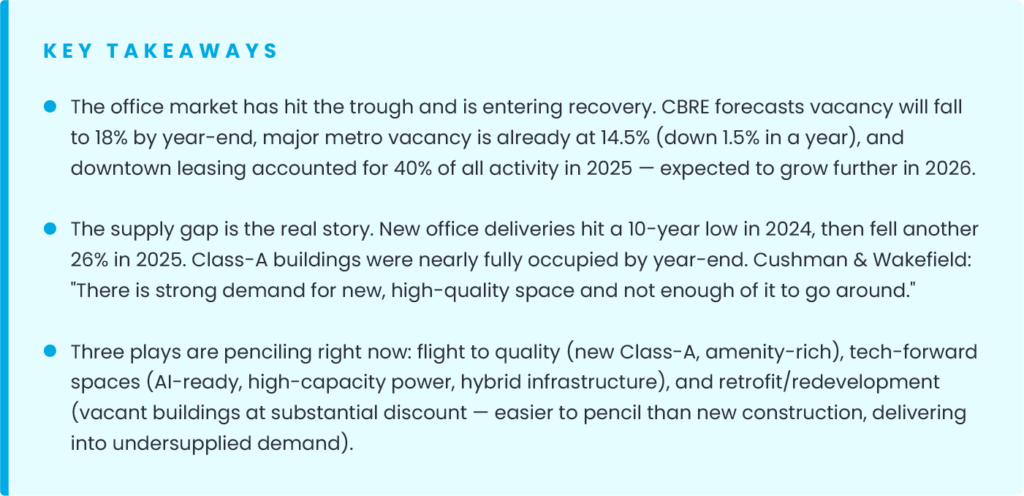

Many experts agree that the office market has hit the trough and is beginning its upswing. Occupier demand for office space is growing; the vacancy rate is declining; and leasing activity this year is expected to surpass 2019 numbers after years of decreasing activity. These are all good signs that the office market is gaining momentum and growing.

Office demand is the center of the story. When occupier demand collapsed during the pandemic, office development and investment equally faltered along with it. Its return is now doing just the opposite. Investors and developers are showing a renewed optimism for the asset class as they see occupiers returning to the deal table. This year, CBRE forecasts the office vacancy rate will fall to 18% by the end of the year, a significant improvement compared to 2024, when CBRE expected the national vacancy rate would still hover around 18.5%.

High-quality assets are leading the conversation. With a vacancy rate of 14.5% in major metros (down a steep 1.5% since the end of 2024) and 13.5% in suburban markets, prime, high-quality assets are helping to revive the market. Major metros are also becoming an important part of the recovery story. After the big city exodus of 2020, companies and employees are returning to the urban core. Last year, downtown leasing activity accounted for 40% of all office leases, and CBRE expects even stronger downtown leasing activity this year. In fact, Cushman & Wakefield’s leasing index shows that gateway markets are trending well above the nation for leasing activity this year, with positive Class-A absorption in 2025.

The slowdown in new construction activity is helping, too. In 2024, new office deliveries fell to a 10-year low, and they continued to decline another 26% in 2025. The absence of new office space has helped rebalance supply and demand and improve market fundamentals, aiding in the overarching recovery. This year, office players will finally start to see a more stable and profitable market.

Opportunities to Build

The post-pandemic downturn in office brought new construction to a halt—but as demand recovers, there are new opportunities to develop office spaces again. After a difficult first quarter, commercial construction began to pick up in April, driven by both office and data center development. However, the office market has shifted. Companies are looking for specific characteristics in an office space today, and developers need to evolve to deliver competitive and relevant properties that will meet current demand.

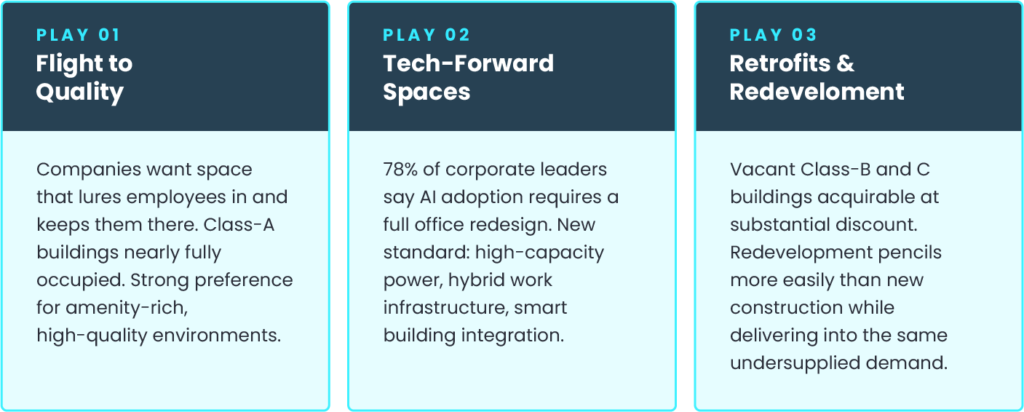

Flight to Quality

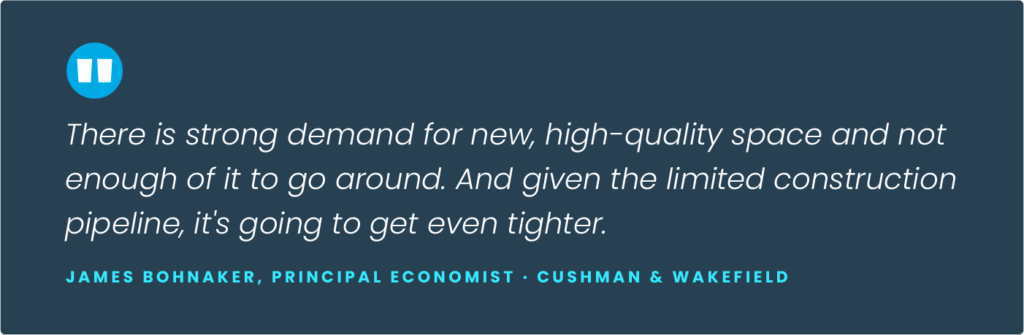

Companies are actively campaigning to get employees back to the office, and they want space that will help lure employees in and keep them there. With home offices, laptops, and email allowing employees to work from anywhere, a modern office must be a place employees want to come. Companies are showing a strong preference for high-quality and amenity-rich spaces. This has become a sweet spot for the office market. At the end of last year, class-A buildings were nearly fully occupied. “There is strong demand for new, high-quality space and not enough of it to go around,” James Bohnaker, principal economist at Cushman & Wakefield, told CNBC. “And given the limited construction pipeline, it’s going to get even tighter.”

Tech-Forward Spaces

Companies are rapidly integrating AI and other emerging technologies, and it is affecting more than workflows and processes. According to a survey of US office users from Steelcase, an office solutions company, 78% of corporate leaders said that AI adoption will require an office space redesign. Companies looking for new or expanded spaces will expect the property to be completely tech-ready and adaptable to emerging technologies. New standard features include future-proof power capability with high-capacity electrical grids, hybrid work infrastructure to accommodate employees that move between spaces, and smart building system integration.

Retrofits and Redevelopment

While Class-A office is vastly outperforming the market, many properties that don’t meet current standards are sitting vacant. Office users have the opportunity to move slowly and be selective, and they aren’t signing leases for spaces that don’t deliver on their needs. This type of discerning demand dynamic has created a real opportunity to redevelop and reposition existing office spaces to meet current needs. Vacant or largely vacant buildings can be purchased at a substantial discount, making redevelopment projects more easily pencil than new construction while still delivering into a highly desirable asset.

As Momentum Builds, Caution Remains

The office market is expanding, but there are still challenges that could derail that progress. Softening in the labor market, for one, could easily offset growing office demand and derail progress. But geopolitical issues, like the conflict in Iran, and tariffs could also impact office-using business performance. Developers should feel optimistic about the progress in the sector, while remaining realistic about the lingering headwinds.

Big picture, the office market has entered its recovery, and with it, there is increased opportunity for investment and development—but the market still has challenges. Developers that are leveraging software programs like Northspyre are able to better scrutinize opportunities, analyze market demand, and run the numbers to determine if the project is viable and will pencil. This is the best option to move forward in the current office environment.