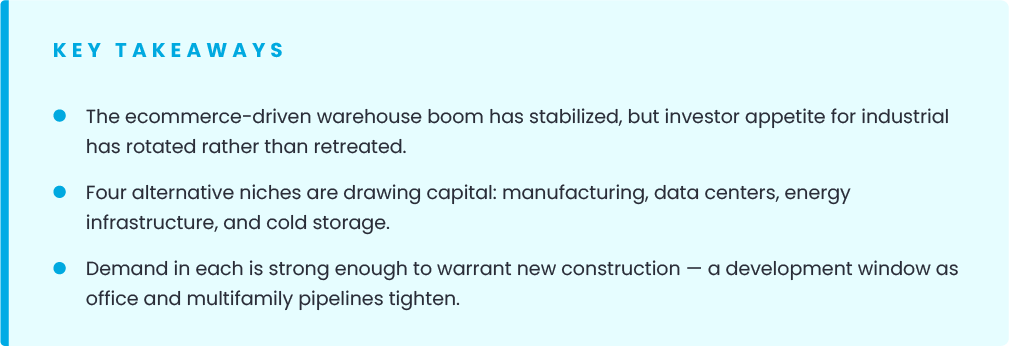

Ecommerce made industrial the darling of CRE. That growth has stabilized — but capital is rotating into four niches strong enough to warrant new construction.

If you can believe it—maybe you’ve only been in the industry for 10 or 15 years—there was a time when the industrial sector was considered an undesirable and unappealing asset class. Since the 2010s, ecommerce has changed the conversation. Industrial facilities transformed from pollution-producing manufacturing facilities into shiny, clean warehouses and last mile logistics facilities that were more comparable to a pseudo-retail property than a traditional industrial facility. Nearly overnight, the industrial sector became the darling of the commercial real estate industry.

But, nothing lasts forever. While warehouse and logistics facilities are still an important part of the industrial vertical, the massive growth of ecommerce has ended and demand has stabilized. However, industrial investors are looking at the industry through a new lens, and they are hungry to continue to invest in industrial properties. Alternative industrial assets that may have been considered unappealing 20 or 30 years ago are getting a new life. A rising tide lifts all boats; ecommerce elevated industrial, and it’s not going back.

Here are the alternative industrial assets that investors are eyeing today, and why developers should take note.

Manufacturing

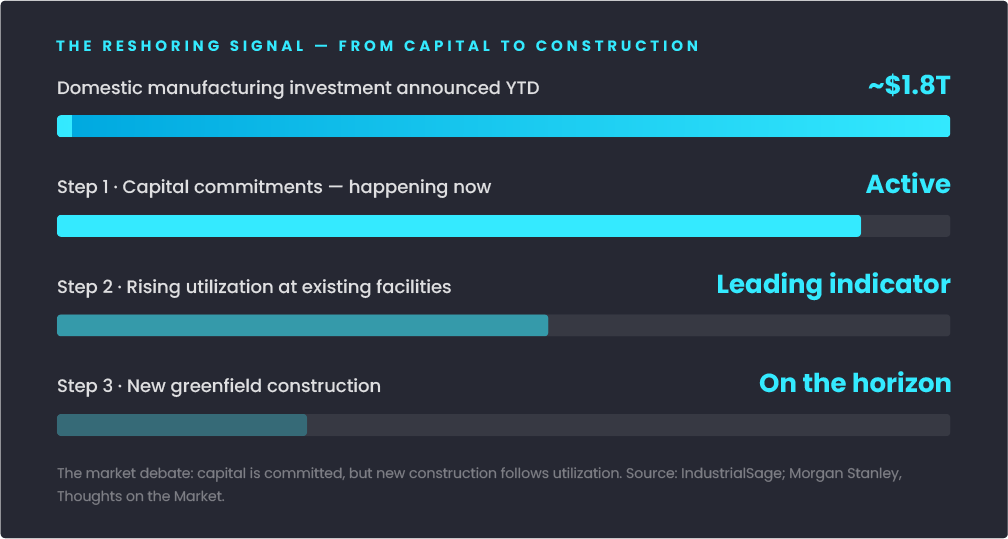

Pro-manufacturing policies have helped the catalyze a wave of new investment in the manufacturing sector. Already this year, companies have announced nearly $1.8 trillion in domestic manufacturing investment. The surge in investment supports the long-term outlook for increased manufacturing development—but when will that demand begin to warrant new construction?

“The big market debate is whether these investments will generate a whole wave of greenfield projects—that is brand new, multi-year construction initiatives to build facilities, factories, and infrastructure from the ground up,” asked Michelle Weaver, U.S. Thematic and Equity Strategist at Morgan Stanley, in the Thoughts on the Market podcast. The answer from U.S. Multi-Industry Analyst at Morgan Stanely: look at the utilization of existing assets. Manufacturing companies will begin to bring production to the US at existing facilities. This will show manufacturing is reshoring, demand is increasing and the need for a new facility is on the horizon.

Data Centers

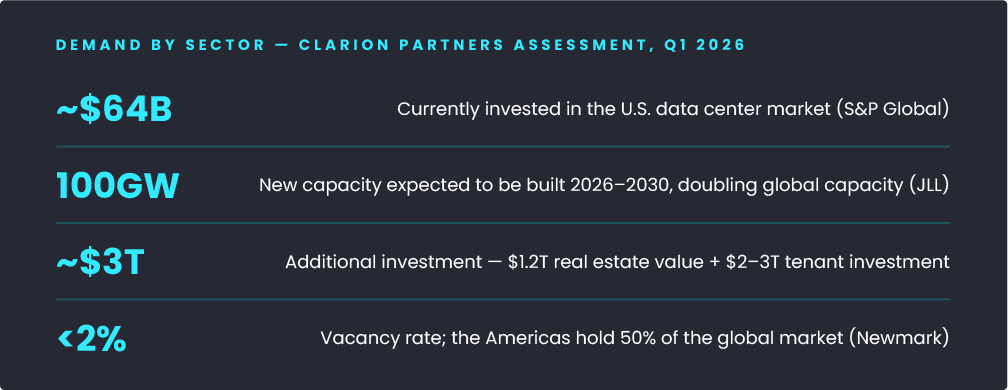

If there was one niche to usurp the spotlight from warehouse and logistics facilities, it is undeniably data centers. Required to support AI adoption at scale, data centers are experiencing unprecedented demand. There is approximately $64 billion currently invested in the data center market, and the demand potential is even higher. JLL estimates that 100GW of data center space will be built between 2026 and 2030, doubling global capacity and representing approximately $3 trillion of additional investment. That figure breaks down as $1.2 trillion in real estate value creation and $2 trillion to $3 trillion of additional tenant investment in the facility.

The data center boom isn’t new. The sector has been surging for the last five years, but the runway for the market is long. With significant requirements for data centers through 2030 and beyond. With a sub 2% vacancy rate, dominance for data centers in the Americas—it represents 50% of the global market—and the continued promise of growth in AI, there is still ample opportunity for new construction in this space.

Energy Infrastructure

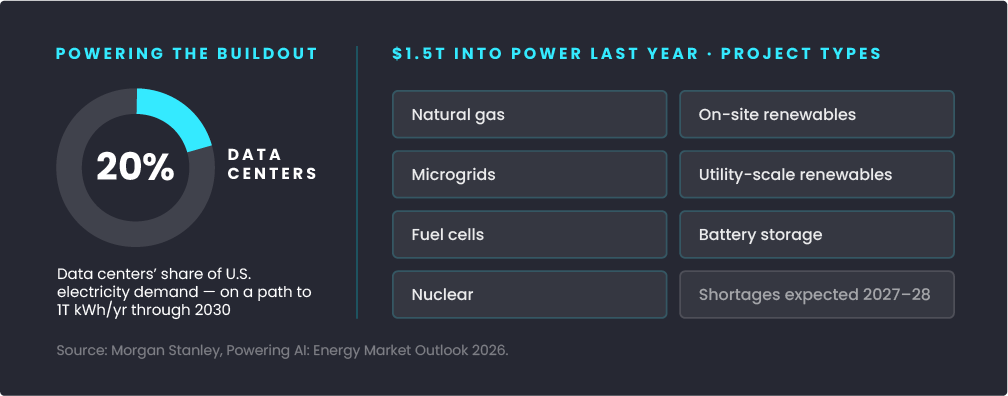

Power is the foundation of data center development, and it is the biggest roadblock to growth in the market. In the data center and technology space, power is, well, power. However, investors in the data center space anticipate significant power shortages by 2027 or 2028. It’s a real concern. Demand for electricity is surging alongside data center development, and it is expected to grow to 1T kWh per year through 2030. Data centers account for 20% of that demand.

Bring Your Own Power Projects are gaining popularity as a result. In these projects, companies are investing in their own off-grid power solutions, like microgrids and self-power generation to support hyperscalers and data centers.

The energy sector is growing in step. Last year, investment in the power industry hit $1.5 trillion. Common projects include natural gas, on-site renewables, microgrids, utility scale renewables, fuel cells, battery storage and nuclear energy, all of which are needed to support future grid capacity required by AI models.

Cold Storage

Another trend in online shopping is fueling growth in the cold storage market. This year, online grocery sales are projected to reach $150 billion. To support this growth, NAIOP research says there is “massive, immediate demand for refrigerated fulfillment infrastructure.” But it isn’t only online grocery shopping. Emerging pharmaceutical treatments, like complex biologics, mRNA-based treatments and advanced cell therapies also require ultracold environments. Together, there is rapidly expanding demand for sold storage facilities. NAIOP reports that cold storage will double in size and reach a valuation of nearly $125 billion in the next decade.

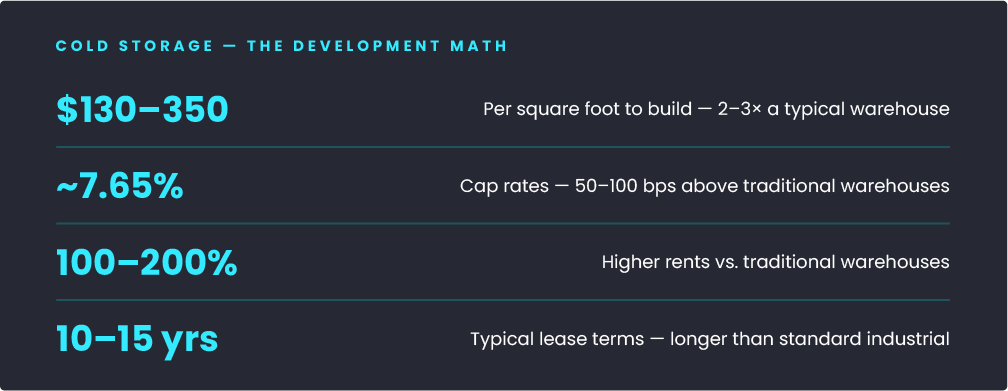

While demand is surging, cold storage is expensive to build. At $130 to $350 per square foot, the cost to build cold storage is two- to three-times higher than a typical warehouse facility. Still, the fundamentals are strong. In addition to rising demand, cap rates sit a 50 to 100 basis points above traditional warehouses at about 7.65%; rents are 100% to 200% higher than traditional warehouses; and lease terms are often longer than a typical industrial lease at 10 to 15 years. The fundamentals make this an attractive development opportunity, even with the higher barrier-to-entry cost.

Development management software, like Northspyre, can help developers manage the higher development costs of cold storage. With financial forecasting and reporting, real-time budget tracking, and proforma modeling, developers can have better control over the total project cost, find efficiencies and trim excess to reduce the overall cost of construction and hit investment targets.

The industrial market is evolving and maturing. While ecommerce businesses launched the sector into the spotlight, today, there is tremendous value beyond the warehousing and logistics space. These four industrial niches are not only attractive investments, but growing demand warrants new construction as well. As construction pipelines tighten in other asset classes, like office and multifamily, these niche industrial assets offer an attractive opportunity for developers.