Published rent growth numbers are masking a decade-low effective rent story. Here’s what developers need to know about concessions, blended rent metrics, and underwriting in today’s multifamily market.

There is a good argument to be made in favor of multifamily development. The nation is chronically underhoused, the for-sale housing market has a high barrier to entry, and interest rates are stabilizing—all good signs that the multifamily market is poised for long-term success. However, multifamily developers are closely watching rent growth trends, and there, the data is a little less encouraging.

It’s obvious that rent growth has slowed and stabilized across the country—but a closer look reveals that the numbers aren’t quite what they seem. In the past year, multifamily concessions have increased dramatically, and the trend is inadvertently skewing rent data and placing a veil over tenant trends. The market dynamic has blinded apartment developers, who need accurate data to underwrite prospective developments and set realistic and achievable pro formas. Here, we take a closer look at rent trends, concessions, and tenant demand, and offer data-backed solutions to set proformas and underwrite new developments.

Multifamily Outperforms Expectations

Overall, the apartment market had a strong first quarter. The vacancy rate notched down 20 basis points to 4.8%, thanks in large part to high net absorption that outpaced the new construction deliveries, according to research from CBRE. Rental rates remained relatively flat, up .2% year-over-year and .4% quarter-over-quarter, but on trend with the historical first quarter averages.

The performance was welcome, albeit unexpected, for multifamily players, who entered the year expecting softening tenant demand and an oversupply while the market absorbed new deliveries. The activity sets the market up for a strong spring. Employment will play a critical role in the rent growth-demand dynamic. While undersupply of housing has helped to fuel demand, weak job and wage growth could alternatively weigh down rent growth. This is the dynamic that is playing out in the first quarter, where demand and absorption are outperforming expectations, but that momentum hasn’t translated into meaningful rent growth.

High Concessions Reveal Possible Strain

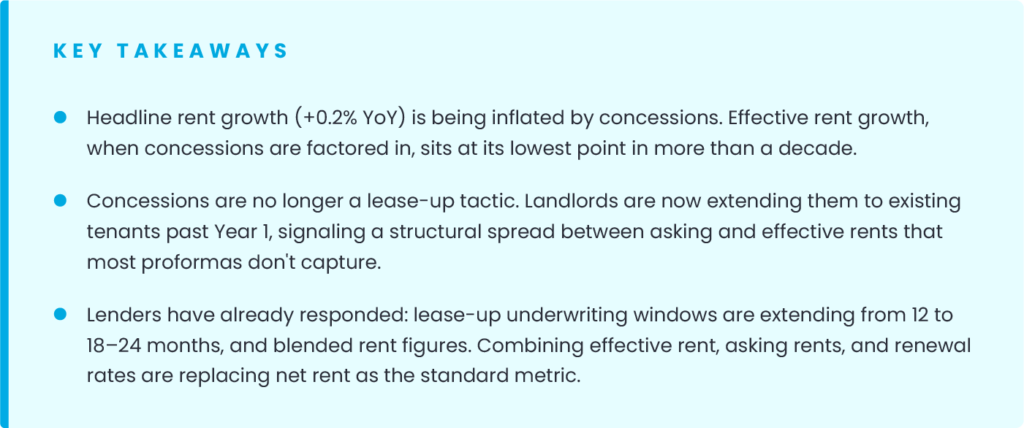

Flat or stabilized rent growth is a caution sign for multifamily developers—but rent trends are likely more distressed than they appear. Reports in April found that 40% of apartment owners are offering concessions to help drive leasing activity. Common concessions include one or more months of free rent, reduced fees, or free extras, like parking. When taking concessions into account, rent growth fell to .2% in the first quarter, the lowest rent growth in more than a decade, according to research from Yardi Matrix.

The Sunbelt region—which has seen the sharpest increase in rental demand, population growth and rent growth in the last decade—is now a hotspot for concessions. In Sarasota, Florida, for example, 81% of apartment properties offer concessions. Other popular Sunbelt destinations, including Austin, Phoenix, San Antonio and Charlotte, are seeing an increase in concessions as landlords compete for tenants. Major markets, on the other hand, are not seeing the same spike in concessions. Big cities like San Francisco and New York City have tight supply, strong demand, and accordingly strong rent growth with limited concessions.

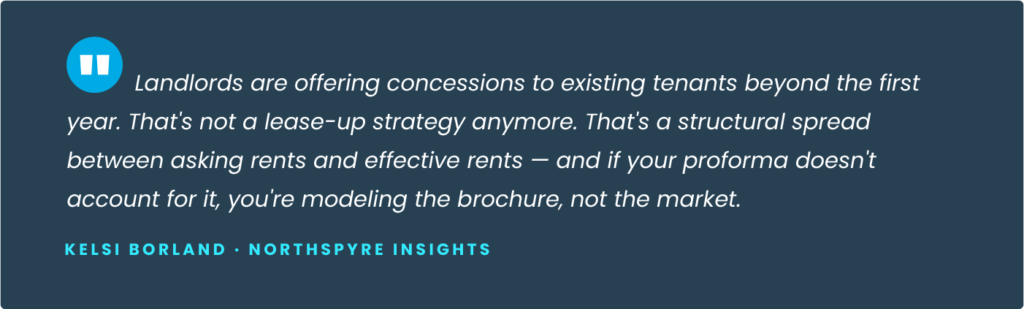

Along with increased concessions, an unusual trend has emerged: landlords are offering concessions for longer. Traditionally, incentives have been used during lease-up to drive occupancy. After the first year, those incentives would expire, and rents would transition to the normal market range. Today, however, landlords are offering perks to existing tenants beyond the first year as a strategy to maintain occupancy. This trend in particular is concerning because it suggests a deeper spread between asking rents and effective rents.

Underwriters Lean on New Metrics

Apartment developers must take a harder look at rent growth to include short- and long-term concessions. They can follow the lead of banks and underwriters, which have started to lean on more robust rental rate figures to better understand income trends. Lenders are using more conservative estimates of effective rent figures—which can be hard to estimate because concessions vary so widely—and many are embedding concessions into future income assumptions. For developers, lenders are applying these policies by extending the lease-up timeline from 12 months to 18 to 24 months.

Effective rent growth, however, isn’t merely replacing net rent growth as the preferred measurement. According to CBRE, a blended rent growth figure is emerging in an attempt to capture the spectrum of different rental rates circulating in the market, including effective rent growth, asking rents and renewal rates. The blended figure gives underwriters deeper visibility into rent trends and allows for better cross-market comparisons.

Tenant Demand Gives the Big Picture

Multifamily leaders are looking beyond raw rent growth to accurately underwrite new developments and acquisitions. Blended rent growth is playing a big role, as noted earlier, but underwriters are also increasingly analyzing tenant demand to understand rent growth and, ultimately, income potential. Underwriters are looking at tenant renewals in particular more closely as part of the rent analysis. Renewals now make up the largest share of lease transactions in today’s market, and they are an important figure in understanding income potential. Grant Harris at Northmarq says that lenders in particular are looking at how concessions are applied to lease renewals. If tenants are renewing without incentives, underwriting standards are less conservative, he says.

Using Data to Hit Proforma Goals

Multifamily developers have always used rent growth to appropriately forecast potential income performance and set an achievable proforma. Today, ancillary data, like effective rent growth, new leases and lease renewals, have made that calculation more complicated. There is simply more data to consider when underwriting and setting a proforma. Thankfully, there are new tools that can help. Northspyre’s advanced modeling algorithms can analyze multiple data sets and unique scenarios to produce an accurate forecast of project cash flow, returns, and equity distributions in minutes. The tool can compare across deals and markets and include past performance information to personalize the results.

Proforma modeling tools like this are the future. As markets become more complex and more metrics are required to vet, analyze, and underwrite a prospective deal, AI modeling is quickly becoming a necessary solution to capture the complete picture and make informed decisions.

Multifamily developers have a lot of reasons to break ground on a new project—and one reason to pause. By understanding the rent data and using a tool like Northspyre’s proforma real estate software, developers can mitigate risk, appropriately underwrite new deals, set achievable proformas, and find healthy returns.