Northspyre Blog

Expert insights & resources

Stay informed with the latest tech trends, industry insights, and best practices for real estate development.

Northspyre Insights

The Beginning of a Pro-Development Era: How Local Governments Are Opening Doors for Developers

Several state and local municipalities have launched pro-development reforms to make it easier…

Northspyre Insights

On Repeat? Inside the Fed’s Decision to Hold Rates in the First Quarter of 2026

Discover the top trends to watch in CRE development acquisitions.

Market Trends, Real Estate Development

The Future of CRE Development Acquisitions: 2026 Digital Trends to Watch

Discover the top trends to watch in CRE development acquisitions.

Real Estate Development, Technology

How to Develop a Strategy-Focused Development Pro Forma for Smarter Real Estate Projects

Learn the ins an outs of development pro forma, with the strategy driven…

Real Estate Development, Real Estate Technology

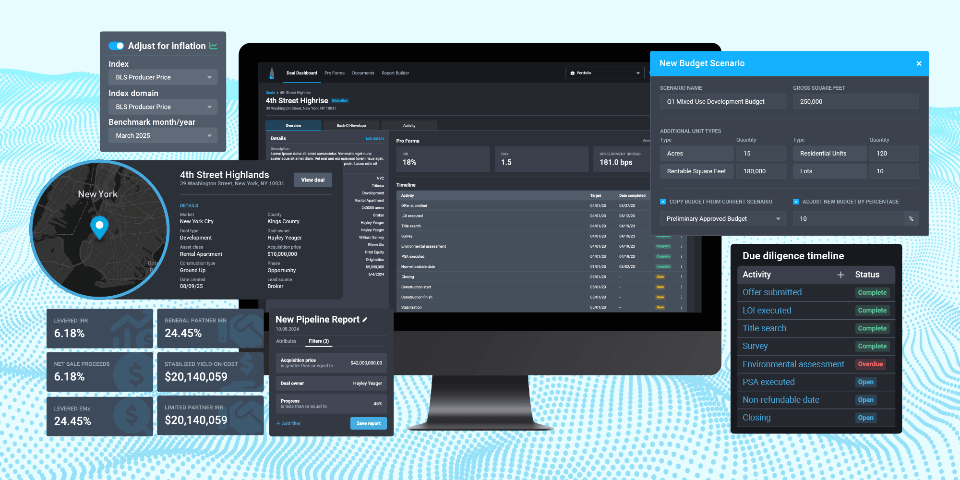

Supercharge Acquisitions & Investment: Introducing Northspyre Deal

Discover how Northspyre Deal keeps teams aligned and accountable across the development pipeline.

Real Estate Development, Real Estate Technology

Mastering the DCF Model for Real Estate: How to Leverage Tech for Better Financial Forecasting

Here's how to master the DCF model for real estate.

Real Estate Development, Technology

Smarter, Faster, More Predictable: How Northspyre Powered Real Estate Development in 2025

A look back at product updates, new features, and achievements in 2025.

Market Trends, Real Estate Development

Why Manufacturing is Taking the Spotlight in Industrial Development

Learn how legislation is boosting manufacturing in industrial development.

Market Trends, Real Estate Development

2026 Trends to Watch in Commercial Real Estate

Here are the top 2026 trends in CRE to watch.

See Northspyre in action

See how leading developers use Northspyre to work smarter at every stage of the development lifecycle.