Commercial real estate investors and developers have been playing the waiting game for the last five years. Market stakeholders have been waiting for the economy to stabilize; waiting for interest rates to come down; waiting for demand to return; and waiting for pricing to normalize. Well, the wait is finally over.

In the first quarter, the commercial real estate market gained momentum, with substantial improvements in investment activity, tenant demand and capital access. Notably, the market’s performance corresponded with expectations at the start of the year, a good indicator of rising stability and professional alignment.

The market is moving in the right direction, and investors and developers have gained the confidence to step off of the sidelines and start transacting. Here is a closer look at the commercial real estate activity in the first quarter.

Investment Activity Ramps Up

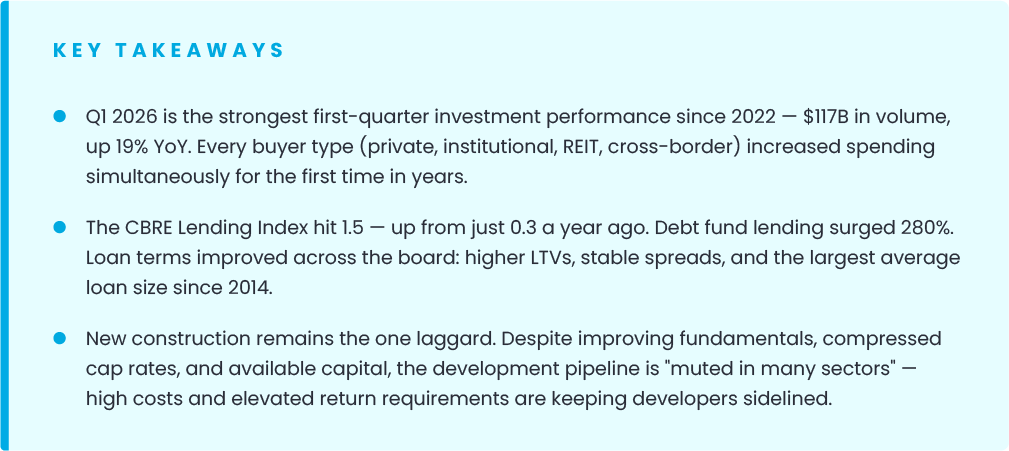

The first quarter 2026 is the best first quarter investment performance since 1Q22, just before The Federal Reserve began aggressively increasing interest rates. Investment volume increased 19% year-over-year, totaling $117 billion. Trailing four-quarter investment volume was even better, up 24% to $534 billion. Commercial real estate investment is a good way to temperature check the market and gain insight into investor sentiment—and sentiment is clearly improving.

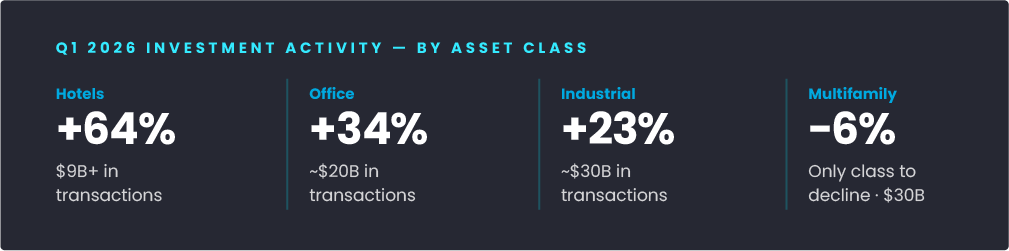

Single asset transactions, which make up the vast majority of investment sales, rose by 13% totaling $87 billion, but portfolio sales and entity-level sales all increased. By asset class, industrial properties led the quarter, accounting for nearly $30 billion in transaction activity, a 23% year-over-year increase. Offices and hotels also saw significant increases in transaction volume, with office up 34% and accounting for nearly $20 billion in sales, and hotels up a whopping 64%, with a total of more than $9 billion in sales. Multifamily was the only asset class to tumble. Transaction volumes fell 6%, but still accounted for nearly $30 billion in transactions.

Deals were largely concentrated in major metropolitans. New York, Los Angeles, San Francisco and Dallas were the top investment markets, with some markets seeing a major uptick in activity. New York investment, for example, was up 37.6%, and San Francisco investment rose 48.3%.

In the first quarter, everyone was buying. Private investors increased spending by 17%, institutional investment was up 23%, REIT activity increased 49% and cross-border investment increased 18%. Even better, institutional investors were net buyers for the quarter.

Lending Market Is Back

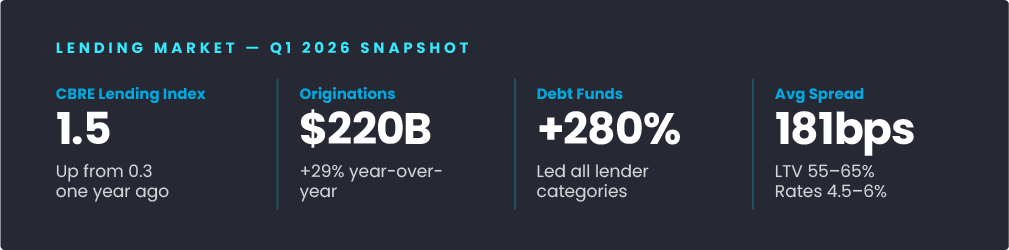

While improved market fundamentals helped fuel the active investment market in the first quarter, the lending market also played a major role in supporting transaction activity. The CBRE lending index increased to 1.5, the highest level since 2021 and a significant increase from a rating of just .3 a year ago. The index tracks loan originations, and a higher score is considered a sign of stronger lending and a risk-on environment.

Loan originations increased 29% in the quarter, totaling $220 billion, but the terms of the loans was the most encouraging. The quarter saw more non-agency loans, stable spreads, higher LTV ratios, and average loan size was the highest since 2014. Refinancing activity accounted for about 68% of loan volumes, according to Newmark.

Looking at non-agency deals, alternative lenders actually led the market, accounting for more than half of closings and increasing activity 19% year-over-year. However, debt funds were the real star. Debt funding lending activity increased 280%, driving the overall increase in originations. Banks, life companies and CMBS lenders were all active in the quarter, but lending volumes for each were down compared to last year.

Spreads tightened across commercial and multifamily loans, with the average spread 181 basis points. The average LTV was 55% to 65%, and interest rates were generally in a 4.5% to 6% range.

Anemic New Construction

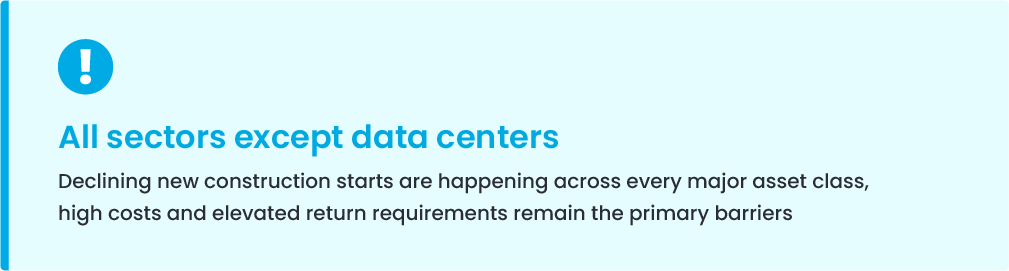

Investment and lending activity gained momentum in the first quarter, but new construction remained anemic. Commercial real estate developers carry a higher risk on speculative projects than investors, and many have not felt confident enough to break ground. Clarion Partners calls the construction pipeline “muted…in many sectors,” despite a broader ongoing recovery.

Declining new construction starts are happening across all asset classes except data centers. Commercial real estate fundamentals have improved considerably in the last two quarters, construction lending is available and cap rates have compressed—all encouraging factors to support new development—but construction costs and elevated return requirements have suppressed new construction activity so far. However, Clarion Partners expects new construction activity to increase over the next several quarters.

Leveraging advanced software tools, like Northspyre’s project oversight programs, can help offset challenging construction costs and elevated return requirements. These tools help open doors for developers to take advantage of improving fundamentals and make projects pencil. Functions like budget tracking, financial forecasting, accurate proforma model all help to illuminate a path to make the numbers work and keep a project on track. These tools can help developers overcome obstacles like high construction costs and hit investment targets.

Demand Boost Across Sectors

Demand is the real cornerstone of commercial real estate market, and it has helped keep the market above water over the last few years as interest rates increased and valuations slipped. Demand continues to thrive and improve across asset classes, supporting NOI growth and helping push cap rate compression. Employment growth and consumer spending will both continue to support healthy demand.

Still, Clarion Partners notes that demand can vary widely across asset classes, and it offers a rating for each asset class. Demand is strong for multifamily assets, data centers, medical office and retail strip centers; medium for industrial assets, malls and hotels; and demand is soft for office, life sciences and self-storage. Morgan Stanely’s market view aligns with varied look at demand, where some sectors are seeing record levels of demand and other areas are softening, but its research also notes the lack of tenant volatility. “The effects of fiscal, monetary, trade and regulatory policy—particularly in the U.S.—should support more predictable occupier behavior and pockets of strengthening demand,” says Morgan Stanley’s first quarter assessment.